June 2018

Monthly Market Summary

June 2018

The month of May started with a positive for the US and global markets as President Trump delayed the controversial trade tariffs for 30-days, giving EU and other allies time to negotiate a trade deal with the US. A high-level delegation was also sent to China for trade talks easing the concerns of a trade war. However, over the month, the markets witnessed intermittent bouts of corrections as the concerns over US-China trade war remained one of the important driving forces for Wall Street. The Asian Pacific remained susceptible to the trade concerns with the China-related stocks being the most affected. Another major source of volatility for Asian Pacific Equity was the geopolitical uncertainty arising from the cancellation of the planned North Korean Talks in Singapore.

Meanwhile, the US Inflation hit the Feds 2% target, the rise in prices was attributed to the economic expansion. The Fed signalled on growing confidence in inflation leading to the strong possibility of rate hikes in June. The threat of inflation and the possible rate hikes by the Fed prompted selling in the fixed income market keeping the yields near the highs of 3%, the fed however held the interest rates steady. The US announced USD 1 billion increase per month in its short-term borrowings, the increase in the long-term borrowing was limited to USD 1 billion per quarter leading to a narrowing differential between the 2-year and 10-year bond yields, a signal of yield curve flattening. The yield differential further narrowed by the end of the month as market speculations rose over trade war and monetary policy outlook intensified.

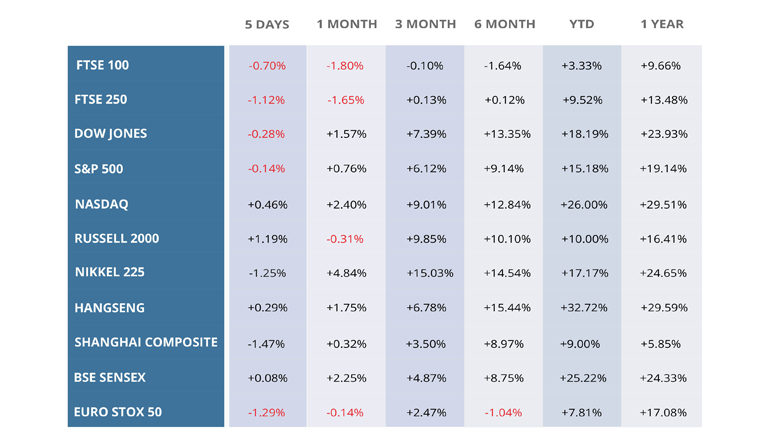

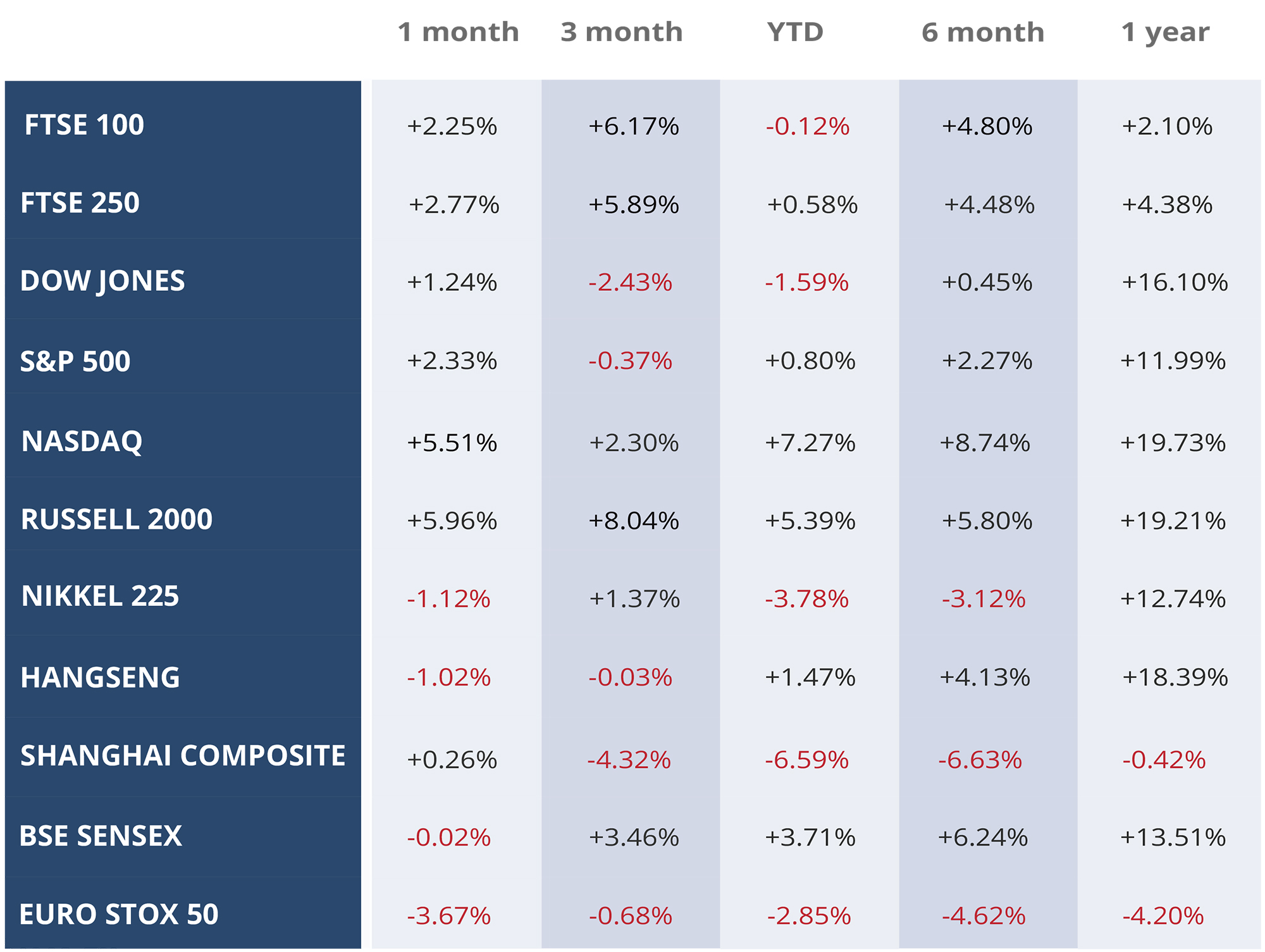

The FTSE 100 was propelled by the rising oil prices to its three-month high in the second week of May with British Petroleum and Royal Dutch Shell accounting for about half of the month’s gain.

The political risk emanating from Italy continued to roil the European markets over the month, with an estimated outflow of USD 4.5 bn from the Western European markets. However, the concerns eased by the end of the month as policymakers in Rome began talks to form a coalition government and avoid snap elections.

The Oil started the month by reaching a four year high of $ 75 a barrel, the prices were driven up by rising demand due to global economic boom and cuts in supply from Open and Russia, in addition to the geopolitical risk arising from the brewing conflict in middle east putting the Iran nuclear deal in jeopardy. However, the prices recovered in the later days of months as reports came out suggesting that the OPEC may wind down production cuts in response to the prospect of reduced supplies from Venezuela and Iran.

The UK pound after reaching the post – Brexit peak last month, took a 3.36% plunge in May, the fall was prompted by the weaker than expected manufacturing data and a weaker outlook for UK inflation. The UK inflation data in the 3rd week of May showed a fall in UK inflation to 2.4%; this was the second consecutive month of drop in inflation.

The US dollar in the early days on May saw a reversal from the weaker outlook as the fears of narrowing policy differentials between the US and Europe, and the US and Japan dissipated as the central banks of Europe and Japan softened their stance on monetary policies.

WEEKLY EQUITY MARKET UPDATE – 06/06/2018

Leave a Reply

Want to join the discussion?Feel free to contribute!